TL;DR:

- Home warranties protect asking prices and reduce time on market by offering buyer confidence. They do not increase the home’s appraised value but help preserve the asking price during negotiations. Proper maintenance combined with warranties maximizes their benefit, especially for aging systems and roofs.

Home warranties are defined as service contracts that cover the repair or replacement of major home systems and appliances due to normal wear and tear. The role of warranties in home value is not to inflate your appraised price. Instead, they protect your asking price, reduce buyer hesitation, and keep negotiations from turning into costly repair credits. For homeowners in South Florida, where roofs take a beating from sun, heat, and storms, understanding how warranties function in a real estate transaction can mean the difference between a smooth sale and a painful price cut.

How do home warranties affect a home's marketability and sale price?

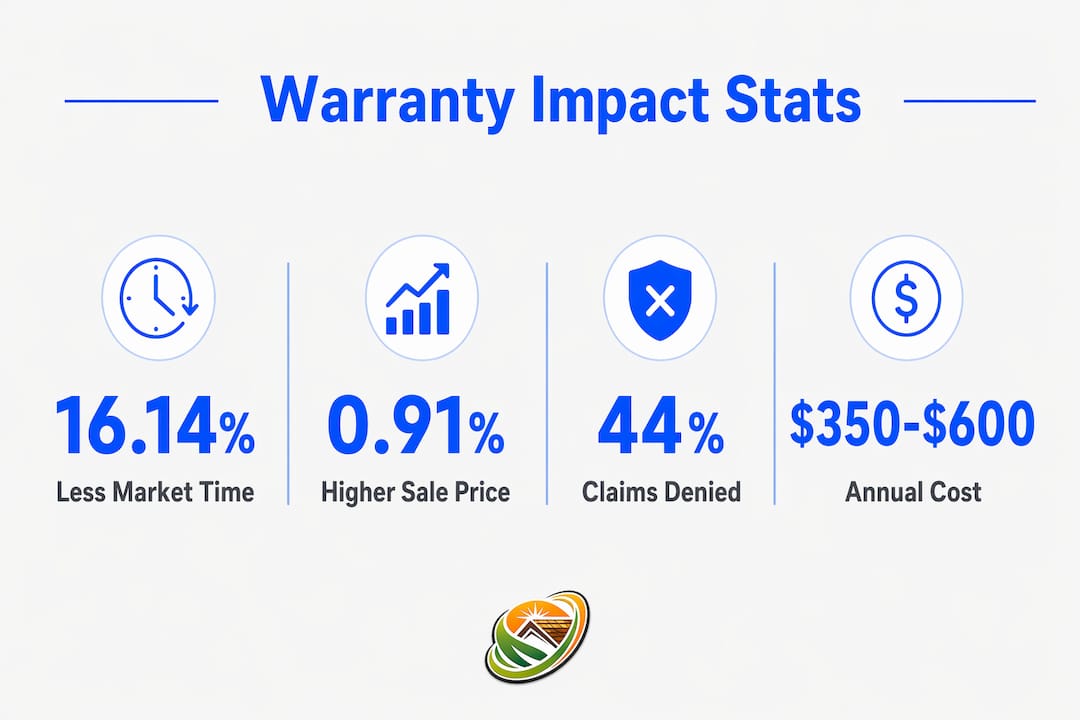

Homes sold with home warranties spend 16.14% fewer days on market and achieve 0.91% higher final sale prices. That may sound modest, but on a $400,000 home, 0.91% translates to roughly $3,640 in preserved value before you even sit down at the closing table.

The reason warranties move homes faster is straightforward. Buyers fear the unknown. A home warranty from a provider like American Home Shield tells a buyer that if the HVAC fails in month three, they are not facing a $10,000 surprise. That peace of mind reduces the urge to negotiate aggressively on price.

Warranties also serve as a negotiation shield during the inspection phase. Without one, a buyer who finds an aging water heater or a worn roof will ask for a repair credit. With a warranty in place, the seller can point to coverage and avoid writing a check at closing. The National Association of Realtors consistently notes that inspection-related concessions are one of the top reasons final sale prices drop below list price.

The impact of home warranties on negotiations is most visible in competitive markets. When two similar homes are listed side by side, the one with a transferable warranty wins more offers. Buyers see it as documented proof that the seller has taken care of the property.

What are the financial pros and cons of purchasing a home warranty?

Annual home warranty costs typically range from $350 to $600, while potential savings for homes with aging systems can reach $1,200 to $3,500. That math looks good on paper, but the real answer depends entirely on your home's condition.

The case for buying a warranty:

- Aging HVAC systems, older water heaters, and worn appliances create genuine financial risk

- A single HVAC replacement can cost $5,000 to $12,500, far exceeding several years of warranty premiums

- Warranties provide budget predictability, replacing unpredictable repair bills with a fixed annual cost

- Homes with aging systems derive the most measurable value from warranty coverage

The case against buying a warranty:

- Well-maintained homes with newer systems often see a net financial loss on warranty premiums

- Approximately 44% of home warranty claims are denied or only partially paid due to wear-and-tear definitions and coverage caps

- Warranties frequently pay depreciated values, not replacement costs, leaving homeowners to cover the gap

- Service fees, exclusions, and coverage limits reduce the real payout on many claims

The depreciation issue is the one most homeowners miss. A warranty company may approve your claim for a failed appliance but pay only the depreciated value of a 12-year-old unit. You still owe the difference between that payout and the cost of a new replacement.

Pro Tip: Before purchasing a home warranty, audit your home's systems. If your HVAC, water heater, and roof are all under 10 years old and well-maintained, the warranty premium may cost more than you will ever recover. Reserve that money in an emergency repair fund instead.

| Factor | Warranty makes sense | Warranty may not pay off |

|---|---|---|

| Home system age | Systems over 10 years old | Systems under 5 years old |

| Annual cost | $350–$600 per year | Same cost regardless of condition |

| Potential savings | $1,200–$3,500 for aging homes | Minimal for newer, maintained homes |

| Claim approval rate | Varies; roughly 56% fully paid | 44% denied or partially paid |

| Best use case | High-risk, older home systems | Well-maintained, newer home systems |

How do roof warranties play a unique role in preserving home value?

Transferable roof warranties provide psychological assurance to buyers but do not directly increase the appraised value of a home. This distinction matters. A roof warranty will not cause an appraiser to write a higher number on your report. What it does is remove one of the biggest objections buyers raise during inspections.

Roof warranties are especially powerful in South Florida, where buyers know the climate is hard on roofs. A transferable warranty from a certified contractor tells the buyer three things: the roof was installed or serviced by a professional, defects are covered, and the coverage moves with the home. That combination removes the intimidation factor that causes buyers to lowball on roof-related concerns.

Here is what a roof warranty does for you as a seller:

- Prevents inspection-based price deductions by showing documented coverage for defects and workmanship

- Serves as proof of maintenance, which builds buyer confidence in the overall condition of the home

- Speeds up the sale by reducing back-and-forth over roof repair credits during negotiations

- Transfers to the buyer, making your home more attractive than a competing listing without coverage

The role of roof warranties in real estate is best understood as a marketing and negotiation tool. Knowing how to transfer a roof warranty correctly in South Florida is a practical step that protects both the seller and the buyer at closing.

Pro Tip: Pair your roof warranty with a recent inspection report. Buyers and their agents respond to documentation. A warranty plus a clean inspection report is a far stronger negotiating position than either one alone.

How do home warranties differ from homeowner's insurance?

Warranties are service contracts covering normal wear and tear, not insurance policies. Homeowners insurance covers sudden, accidental damage such as a tree falling on your roof or a fire destroying your kitchen. These two products solve different problems, and confusing them leads to real financial pain.

The practical differences break down clearly:

- Coverage trigger: Warranties activate when something wears out over time. Insurance activates when something is suddenly damaged or destroyed.

- Claim process: Warranty claims require a service fee, a contractor visit, and approval from the warranty company before any work begins. Insurance claims go through an adjuster and typically move faster for major damage.

- Payout structure: Warranties often pay depreciated value with coverage caps. Insurance pays replacement cost value on most modern policies.

- Exclusions: Warranties exclude pre-existing conditions, improper installation, and items outside the coverage list. Insurance excludes gradual wear, flooding (without a separate flood policy), and maintenance failures.

Home warranties do not guarantee quick or full repairs. Diagnostic delays, contractor scheduling, and partial payments are common. Homeowners who expect warranty coverage to work like insurance end up frustrated and out of pocket.

Pro Tip: Read the exclusions section of any warranty contract before you sign. The coverage list tells you what is included. The exclusions section tells you what will actually get denied.

What practical steps should homeowners take when evaluating a warranty?

Getting a professional home inspection before purchasing a warranty is the single most important step. Pre-existing condition exclusions are a leading cause of claim denials. An inspection documents the current status of your systems and gives you a clear picture of what a warranty will and will not cover.

Beyond the inspection, these steps protect your investment:

- Match warranty coverage to your home's actual risk. A 15-year-old HVAC system warrants coverage. A 3-year-old system probably does not.

- Check transferability terms. A warranty that transfers to the buyer at closing adds real marketing value. Confirm the transfer process and any associated fees before listing.

- Review coverage caps. Many warranties cap HVAC replacement at $1,500, while actual replacement costs run $5,000 or more. Know the gap before you rely on coverage.

- Use warranties strategically in negotiations. Offer to include a one-year warranty as a seller concession instead of a repair credit. It costs less and signals good faith.

- Monitor covered systems proactively. A warranty is not a substitute for maintenance. Keeping systems serviced reduces the chance of a claim denial based on neglect.

Understanding roof warranty options in your region helps you choose coverage that actually fits South Florida's climate demands. The value of home protection plans comes from using them correctly, not just owning them.

Key Takeaways

Home warranties preserve asking price and reduce time on market, but they do not increase appraised value. Their real power is in buyer confidence, negotiation leverage, and financial risk management for homes with aging systems.

| Point | Details |

|---|---|

| Warranties protect price, not appraisal | Warranties reduce inspection concessions but do not raise your home's appraised value. |

| Market time drops with warranties | Homes with warranties sell 16.14% faster, giving sellers a real competitive edge. |

| Claim denials are common | Roughly 44% of claims are denied or partially paid; read exclusions before buying. |

| Roof warranties are negotiation tools | Transferable roof warranties remove buyer objections and document maintenance history. |

| Home condition determines warranty value | Aging systems benefit most; well-maintained homes often see a net loss on premiums. |

What I have learned about warranties and home value after years in the field

Warranties are risk management tools, not investment products. That framing changes everything about how you should use them.

Most homeowners I speak with either overestimate what a warranty covers or dismiss warranties entirely because of a bad claim experience. Both reactions miss the point. A warranty does not make your home worth more on paper. What it does is protect the number you have already earned. In a competitive market, that protection is worth real money.

Roof warranties are where I see the biggest misunderstanding. Homeowners assume a roof warranty will boost their appraisal. It will not. What it does is stop a buyer from shaving $8,000 off your asking price because they are nervous about the roof's age. That is a different kind of value, and it is just as real.

The homeowners who get the most out of warranties combine them with genuine preventive maintenance. A warranty on a neglected roof is a claim waiting to be denied. A warranty on a well-maintained, recently renewed roof is a marketing asset that closes deals. The best approach is always to maintain first, then protect with coverage.

— Daniellison

Protect your roof before the warranty has to work

A warranty covers what goes wrong. Preventive maintenance reduces how often things go wrong in the first place. For South Florida homeowners, that distinction matters most when it comes to the roof.

Shingleroofrenewal specializes in roof preservation using certified Fresh Roof Green Soy Technology, which restores shingle flexibility and extends roof life before replacement becomes necessary. A preserved, well-documented roof pairs directly with a transferable warranty to give buyers confidence and sellers negotiating power. If your roof is showing signs of wear, a free roof inspection from Shingleroofrenewal tells you whether renewal is an option before you spend $15,000 or more on replacement. Call us before you call the roofer.

FAQ

Do home warranties increase a home's appraised value?

No. Warranties do not increase appraised value but they reduce inspection-based price concessions and help sellers preserve their asking price during negotiations.

How much does a home warranty cost per year?

Annual home warranty costs typically range from $350 to $600, with potential savings of $1,200 to $3,500 for homes with aging systems.

Why are so many home warranty claims denied?

Approximately 44% of claims are denied or partially paid because of pre-existing condition exclusions, wear-and-tear definitions, and coverage caps that limit payouts.

Is a roof warranty the same as homeowner's insurance?

No. A roof warranty is a service contract covering workmanship defects and normal wear. Homeowner's insurance covers sudden, accidental damage like storm impact or fire.

Should I get a home inspection before buying a warranty?

Yes. A pre-warranty inspection documents the current condition of your systems and reduces the risk of claim denials based on pre-existing conditions.